Welcome to The Owner's Box!

Life Lessons from the Shifts of Main Street and the Oracle of Omaha

For those who are just joining — Welcome to “The Owner’s Box!”

My name is Peter Boumgarden, and I am a Professor and Director of the Koch Center at WashU in St. Louis. In addition to the newsletter “A Rich Life” that I write with friends, Daryl Van Tongeren and Abram Van Engen, I write and produce a podcast on ownership, which I bring to you here.

In our most recent episode — the first of our second season — we walk you through a big national research and policy project we ran this year in collaboration with the Brookings Institution.

Our research explored the significant and accelerating shifts of ownership in privately held companies all around the US, and what that means for the economic and cultural fabric of the nation. While you can read about that report here, perhaps more interestingly for a Thanksgiving weekend, you might enjoy listening to our 35-minute podcast episode below.

While I met and connected with many of you before I started my work in and around ownership, I believe you will find many shared themes in this work that perhaps drew you to my initial newsletter — “Towers to Bridges.” While not all of us are business owners in the narrow sense, the human drama of shared ownership and the strategic challenges of doing it all well have lessons for us all.

Consider the following from my friend and collaborator on this project, Aaron Klein. Here, Aaron reflects on stage in DC on the potential value of ownership as a vehicle for democratization:

The last point I want to make is an employee point, which is that the American dream is to climb the ladder and to have some amount of ownership and ownership society. And I think that a lot of the reforms we're doing is about democratizing ownership. And the stock market model of democratizing ownership, I think is is a failing model. It's a 20th century model. It's a model that isn't working. When you can take companies in the modern era and go massively large without ever going public. And where you're finding more and more of a winner take all economy, even as economic platforms are to democratize success, you're seeing more things come up in a winner take all world. And this allows employees to benefit in that at one point, the ratio of CEO to janitor pay was much more narrow. The social and cultural norms that kept that have disintegrated to a large degree. You can fight to bring them back. That's kind of you know, I'm intellectually with you that the hill that you're climbing there is pretty steep. Or you can say, how do we make sure the janitor owns a little bit of this company? That to me feels like a much easier path to try and reduce the wealth and income inequality and create greater opportunities for folks across the employee pay scale.

The Shift of Place Over Time

In my personal reflections on this work, I kept turning my attention to how much a place can change as ownership shifts.

Let me give you one example. This week, I am back home in Naperville, IL, celebrating the Thanksgiving holiday with family. I write this newsletter from the library I visited when I was growing up — cue up, deep nostalgia.

That said, the view outside this window has changed drastically in the 20+(!) years since I lived here full-time. Some shops are long gone. CeeBee’s Fine Grocery has long since transitioned into a block of specialty stores, one that includes an Apple Store with lines around the street. Some remain the same name but are clothed in new skin. Anderson’s Bookshop, the first real job for my sister in high school, is still family-owned at 143 years old, with the 5th generation Becky having recently bought the company from her brothers.

For owners like Becky or citizens like you and me, where is meaning found in these transitions? How might we better balance a desire for continuity with the inevitability of change?

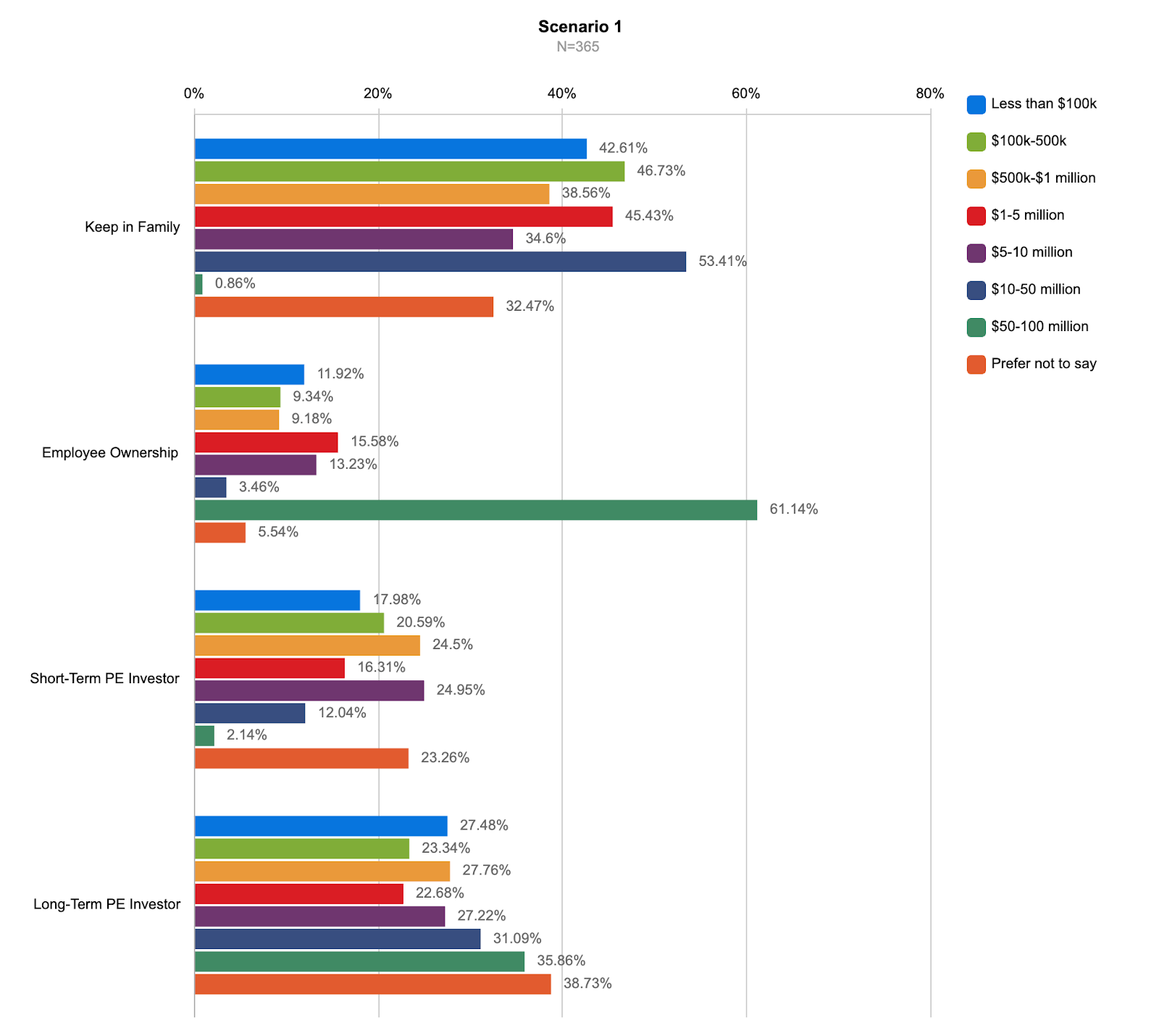

For the owners themselves, one source of meaning in these transitions is found in what the business transitions to. As a part of this Brookings project, we partnered with Enova International, US Bank, and Edward Jones to map the preferences of 600 current business owners of various sizes. By asking them a repeated set of questions on whether they preferred one type of buyer over another, we were able to reveal what was meaningful in this kind of significant change.

Perhaps not surprisingly, for this group — price mattered … a lot! You built something meaningful, yes, but a good part of that value is in the financial value of the enterprise itself.

But so, too, there were other considerations. For example, beyond price (37.5% of the motivation in choice), owners also cared about who would be stewarding the company moving forward (27.5% of the motivation). Not all buyers are created equal.

Take a look at a snapshot of that data below. The image below uses the initial data to simulate how these 600 owners might approach offers from four hypothetical buyers — keeping in the family, transitioning to employees (ESOPs), or selling to a shorter or longer-hold private investor.

For many owners, their hope in the transition was to keep the company in the family. For others, especially owners of organizations over a certain size ($50-100M), it was really appealing to have their company transition to employees (see the big green line that reaches far to the right).

Beyond who is doing the buying, time also seems to matter. Note the allure toward a private investor that is likely to hold the company for a long term versus those likely to flip more quickly. The latter point is part of why we are running in partnership with Brent Beshore at Permanent Equity, the WashU Endowment, and leaders at Broadview Group Holdings a national case competition exploring how one might invest with an eye toward a long-term hold. Think of one model of this as being Warren Buffet and his hope to invest in many of these companies “forever.”

The Power and Peril of Legacy

I suppose that many of these motivations for extensions of one’s impact into the future are linked to legacy. After all, the flip side of legacy is the all too true realization of our mortality and one’s limited ability to leave a lingering imprint on even the most important parts of our lives.

I can’t help but sit in Naperville today and realize how much this town doesn’t depend on me (shocking I know!). It has changed. Evolved. It is not the Naperville I knew when growing up.

The same is true for the friends we have — the family we sit with — and, indeed, the businesses we start. Still, there is something about our deep-seated desire for legacy that hits at a profound human need to matter.

But isn’t there also wisdom in allowing things to become something else? Even those who plan to hold something forever — an investment firm or many of the company owners I have gotten to know through the Tugboat Institute, for example — have to deal with the inevitability of change.

Lessons from the Oracle of Omaha

Just this morning, my good friend Spencer Burke emailed a group of us the letter Warren Buffett sent out about an update to an estate plan and the transitions of the shares of Berkshire Hathaway to his kids.

Listen to the wisdom in Buffett’s acknowledgment of the transiency of life and how it shapes how he thinks about the future of that organization:

Father time always wins. But he can be fickle – indeed unfair and even cruel – sometimes ending life at birth or soon thereafter while, at other times, waiting a century or so before paying a visit. To date, I’ve been very lucky, but, before long, he will get around to me.

There is, however, a downside to my good fortune in avoiding his notice. The expected life span of my children has materially diminished since the 2006 pledge. They are now 71, 69 and 66.

I’ve never wished to create a dynasty or pursue any plan that extended beyond the children. I know the three well and trust them completely. Future generations are another matter. Who can foresee the priorities, intelligence and fidelity of successive generations to deal with the distribution of extraordinary wealth amid what may be a far different philanthropic landscape? Still, the massive wealth I’ve collected may take longer to deploy than my children live. And tomorrow’s decisions are likely to be better made by three live and well-directed brains than by a dead hand.

As such, three potential successor trustees have been designated. Each is well known to my children and makes sense to all of us. They are also somewhat younger than my children.

But these successors are on the wait list. I hope Susie, Howie and Peter themselves disburse all of my assets.

In Buffett’s words, he offers earned trust for things he has built, but so too, Buffett suggests a willingness to forgo control far into the future — something that he might be uniquely capable of grabbing.

Few of us have Warren Buffett-like resources, but there’s much to learn from the Oracle of Omaha about stewarding the resources we do have—financial and otherwise. Can we, like Warren, remain deeply attuned to the power of legacy while resisting the all-too-human temptation to prioritize control at any cost?

I hope you continue to read and listen along as we explore all the ways that ownership impacts us all. Happy Thanksgiving to you and yours!

Looking back at Season 1

If you are new to the podcast or newsletter, we wanted to point you back to every episode of Season 1, linked below. We hope you enjoyed the season, and do share with those who you think would enjoy it!

Episode 1 - Transitioning with Soul with Danny Meyer, Ari Weinzweig, and Bo Burlingham

Tactics Episode 1 - Succession

Episode 2 - Creative Control with Jeremy King

Tactics Episode 2 - Social Discount

Episode 3 - The Beautiful Game with the Taylor Family.

Tactics Episode 3 - The Psychology of Legacy

Episode 4 - Creativity and Continuity with Stuart Weitzman

Tactics Episode 4 - The Four Critical Questions of Ownership

Episode 5 - Brothers in the Vineyard: Growing Fraiche Wine Group

Tactics Episode 5 - The Discipline of Long-Run Ownership

Episode 6 - All That We Bring to the Table with Cindi Bigelow

Peter, with respect to the democratization of ownership, I suspect you are familiar with the works of both Hilaire Belloc and G.K. Chesterton, the fathers of distributism, one of the worst-named concepts ever. The distributists argued that socialism and industrial capitalism (the only kind of capitalism the modern world has known) were two halves of the same coin--a coin in which the means of production were owned by the few (either the state in socialism or the few industrial capitalists) and the mass of people in both systems were proles who end up selling their labor to either the state or the capitalists.

The Chesterbellocs argued for an economic system that incentivized the broad distribution of capital, not through confiscatory redistribution (as the name might imply) but primarily through a thoughtful tax system.

Their heirs at the Society of G.K. Chesterton made an attempt a few years back to re-coin the term as 'Localism,' which at least has the virtue of not scaring people away, but nevertheless it remains a relatively little-known concept. I commend Belloc's introductory book, The Restoration of Property, to you and any of your readers interested in learning more.

As always, appreciate your perspective and that of your co-belligerents in this newsletter.

Cheers!